Netflix and Chill

Welcome to the Schmoozeletter Blog. Your source for weekly water cooler wisecracks from the world of finance. If you have an opinion different than mine or a topic you want to hear about, let me know!

This week, we’re talking about:

Netflix and Chill

People are always wondering what’s the best investment advice around. How do I get a portfolio to the moon?

Do the kids still say “to the moon”?

Yes, yes.

I’m frequently inundated with correspondence about how most effectively to secure the bag of tendies.

Nailed it.

And what I say…

Usually after some sick kickflips…

Is you just gotta:

Chill

To paraphrase the ukulele-strumming GOAT, you just want to invest in the very businesses when they are at reasonable valuations and then do nothing. Hold them for as long as they remain great businesses. Ideally, hold them for a lifetime. Just…

Chill…

Netflix, NFLX, is an exceptional business.

I am not just saying that because every girl between the ages of 4–14 was a K-Pop Demon Hunters character for Halloween this year.

I say that because of their thus-far successful ongoing quest for world domination.

US and Canada?

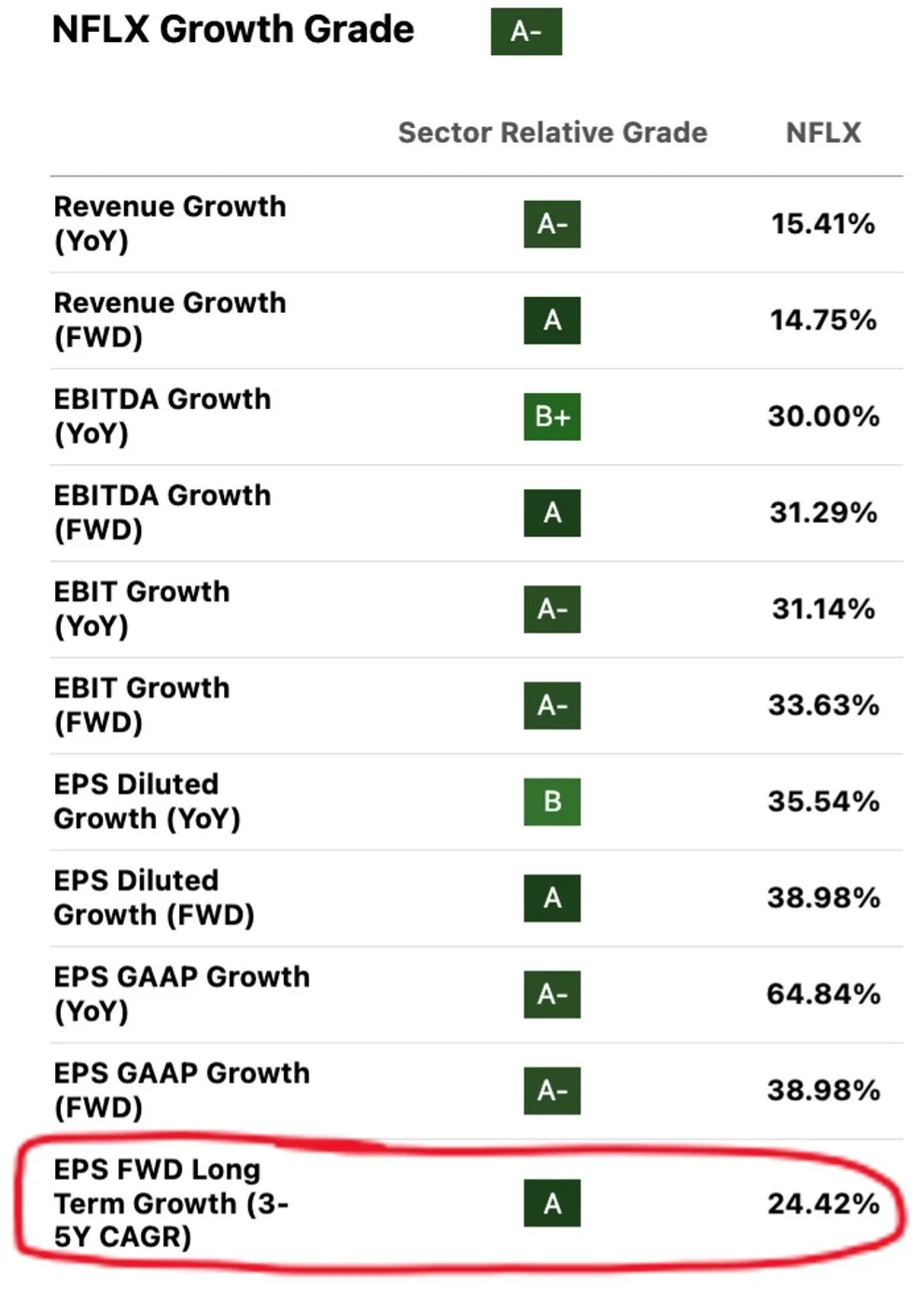

Rapidly growing revenue.

Europe, Middle East, Africa?

Rapidly growing revenue.

Latin America?

Rapidly growing revenue.

Asia Pacific?

Rapidly growing revenue.

Over 300M subscribers as of last December.

And all of them are excited to complain the Stranger Things finale won’t be as good as the old seasons.

The big critique of NFLX a few years ago was they’re on a “hamster-wheel model.” Whatever new money comes in needs to be spent on more content to get more new money.

Which is one of the “ChatGPT is killing Google Search” type criticisms that sound nice until you look at the actual data.

The content budget is growing at half the rate of the revenue.

NFLX isn’t like every AI and tech company that needs to pour money into building an infrastructure of the latest chips and GPUs and fancy whatchamahoozits either. The content budget is the major expense.

Do we know what happens when revenue expands faster than expenses?

The cash comes flowing in.

It is really hard for competitors to keep up when NFLX has this good of financials while having:

1. One of the cheapest prices

2. One of the biggest and most diverse content offerings

Now, you might be thinking:

I’m supposed to believe giving hundreds of millions to Jake Paul is a brilliant business model?

Or

The Electric State was an abomination.

Or

NFLX has fine top-line growth, but it’s just not trading at a multiple I’m comfortable with.

And that is fair. I wouldn’t say that it is cheap with the P/E ratio in the 40s. But with the expected growth, it isn’t exactly expensive either.

When you have an exceptional company trading at a fair valuation, it is generally a good idea to pull the trigger and then do nothing. Push the button then sit back and watch it go. Keep it simple. Keep it casual. Just…

NFLX and chill.

Final Thought

How’s everyone’s crypto wallets doing?

Hate to burst your bubble, but the bubble gonna burst

If you ain’t heard it before, let me be the first.