The Retirement Plan

Welcome to the Schmoozeletter Blog. Your source for weekly water cooler wisecracks from the world of finance. If you have an opinion different than mine or a topic you want to hear about, let me know!

This week, we’re talking about:

The Retirement Plan

Do you know when you can retire?

Do you know what your retirement portfolio should look like?

Do you only know Roth as the front man from Van Halen?

I am usually talking about how to get to retirement, but what do you do if you are close? What do you do if you are there?

All the answers and more in:

The Retirement Plan

So you’ve been working and saving and contributing to your 401(k) and your IRA, and it’s looking like you’ve made it to the top of the mountain.

How do you know if you can call it quits and start living off your nest egg?

You may have heard of the 4% rule. Slowly withdraw 4% per year and cross your fingers you don’t retire into a market downturn that blows up your account, leaving you broke in ten years.

That is certainly one method.

But I have a better method for you. And it is twice as good as the 4% rule.

I call it:

The 8% rule.

Ask yourself:

Can you live off an annual salary of 8% of your nest egg?

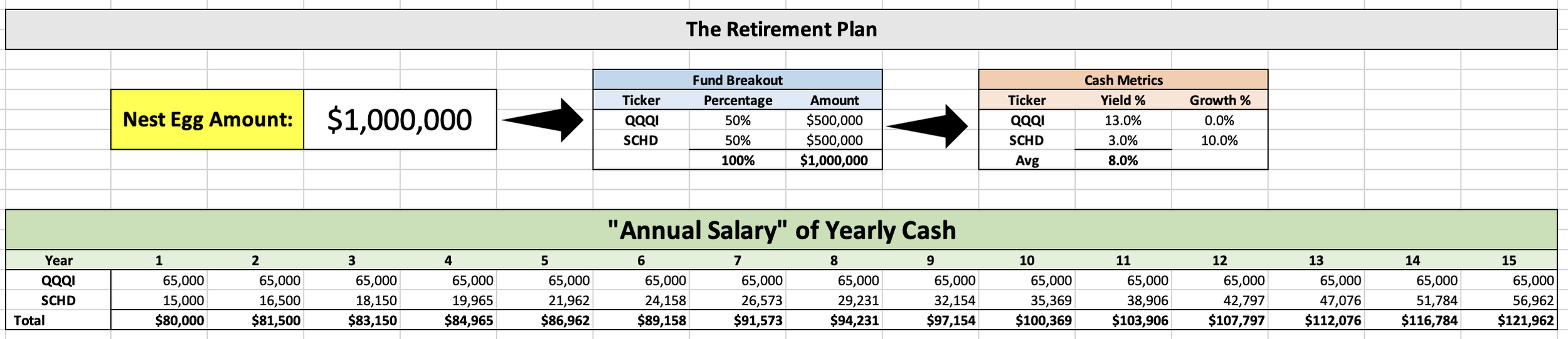

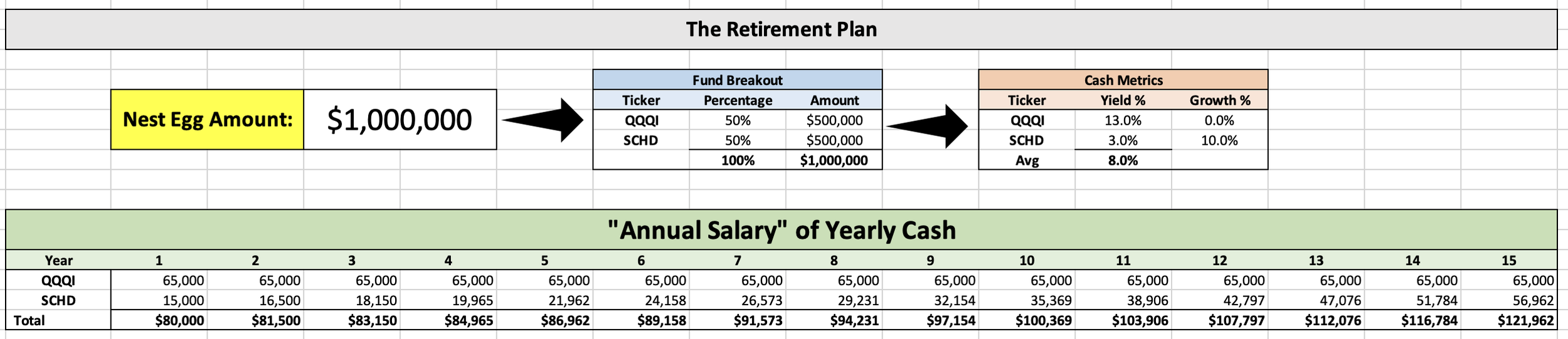

Let’s say you have a nest egg that is $1M.

$1M * 8% = $80k

Can you live off an annual salary of $80k?

Let’s say you have a nest egg that is $2M.

$2M * 8% = $160k

Can you live off an annual salary of $160k?

You get it. Math.

But I am not just talking about selling off 8% per year and hoping for the best.

I am talking about buying into a portfolio that generates 8% per year in cash without selling any principal.

Not only that, but the payments grow annually, so your new cash salary gets a raise every year.

Not only that, but the payments grow at a rate faster than inflation, so your dollar goes farther every year.

You basically switch over to this portfolio one time, then you are set for the rest of your days. You can sit on the beach in the Bahamas and collect your new paychecks.

Introducing:

Dave’s Proprietary Portfolio Using the Dow Jones Dividend 100 Passively Managed Index Fund Through Charles Schwab and The Nasdaq 100 Actively Managed Covered Call Exchange Traded Fund from NEOS*

*Working title.

In layman’s terms, you put your nest egg 50/50 into two funds:

SCHD – A dividend growth ETF

QQQI – A covered call ETF

One fund has low yield but high growth. The other has high yield but low growth.

Together the math works out like this:

Two funds only? Isn’t that risky?

The short answer is no.

SCHD is one fund, but it tracks an index of around 100 stocks that are diversified across every sector. They have the best dividend fundamentals in aggregate in the market.

So SCHD risk level = NOT RISKY AT ALL

QQQI is one fund, but it tracks an index of around 100 tech-heavy stocks and overlays the most common options strategy to generate monthly cash. They use out-of-the-money call options to preserve net asset value.

This one is more volatile by the nature of tech stocks being more volatile, but not very risky in aggregate.

So QQQI risk level = MILDLY RISKY

Together, the portfolio is diversified over 200 stocks across every sector across virtually the entire market.

Also, take a look at where your cash is coming from in year 15:

The first year, 80% of your annual salary is coming from QQQI. But in year 15, your annual salary is roughly 50/50 from QQQI and SCHD.

The “riskier” QQQI starts out doing the heavy lifting for your annual salary. As time goes on, the “safer” and faster-growing SCHD eventually catches up and will soon surpass the cash payment from QQQI.

So your annual salary gets safer and safer every year!

Is it risky?

Combined Portfolio = NOT RISKY

What if I’m in a 401(k) or IRA?

No matter what type of retirement account you are in, the big difference is whether it is:

ROTH or TRADITIONAL

ROTH means no taxes. Congrats! Invest in these two funds, withdraw cash every month tax-free, and live happily ever after.

TRADITIONAL means taxes. Uncle Sam needs his.

What to do and what taxes you pay will depend on the individual situation, but depending on how long you plan to live, you are probably better off converting that TRADITIONAL to a ROTH.

Here is the not-so-fun part:

Converting to a ROTH means one big ol’ tax bill when you convert. One huge hunk of your nest egg gone just like that.

But you never pay taxes again forever.

Keeping it in a TRADITIONAL means you will pay taxes every year forever. And you can’t skirt them by keeping it in the IRA as long as possible because the government makes you take required minimum distributions to get their taxes.

Think of it this way:

If you live for another hundred years, converting to a ROTH and paying no taxes on a growing annual salary for 99 years would be the best decision you ever made.

If you die the day after the conversion, then you would have paid less in taxes keeping it in a TRADITIONAL.

So if you plan on sticking around until your grandkids are adults, you are better off biting the bullet and paying the hefty tax bill in year 1 to get it out of the way.

What if I have a pension or Social Security?

Then you are most likely a baby boomer. Congrats! The way things stand now, you are the last generation that can count on those.

The rest of us will need to invest and rely on our portfolios.

But if you are receiving a pension or annuity or some other payment, you simply add that into your new annual salary, and your equation looks like this:

If Annual Salary + Pension/Social Security/etc. > Annual Cost of Living =

What if you are years from retirement and these numbers sound astronomical?

Millions of dollars?!

So I gotta be Bezos if I ever want to live off my investments?

No.

Not as long as you consistently invest.

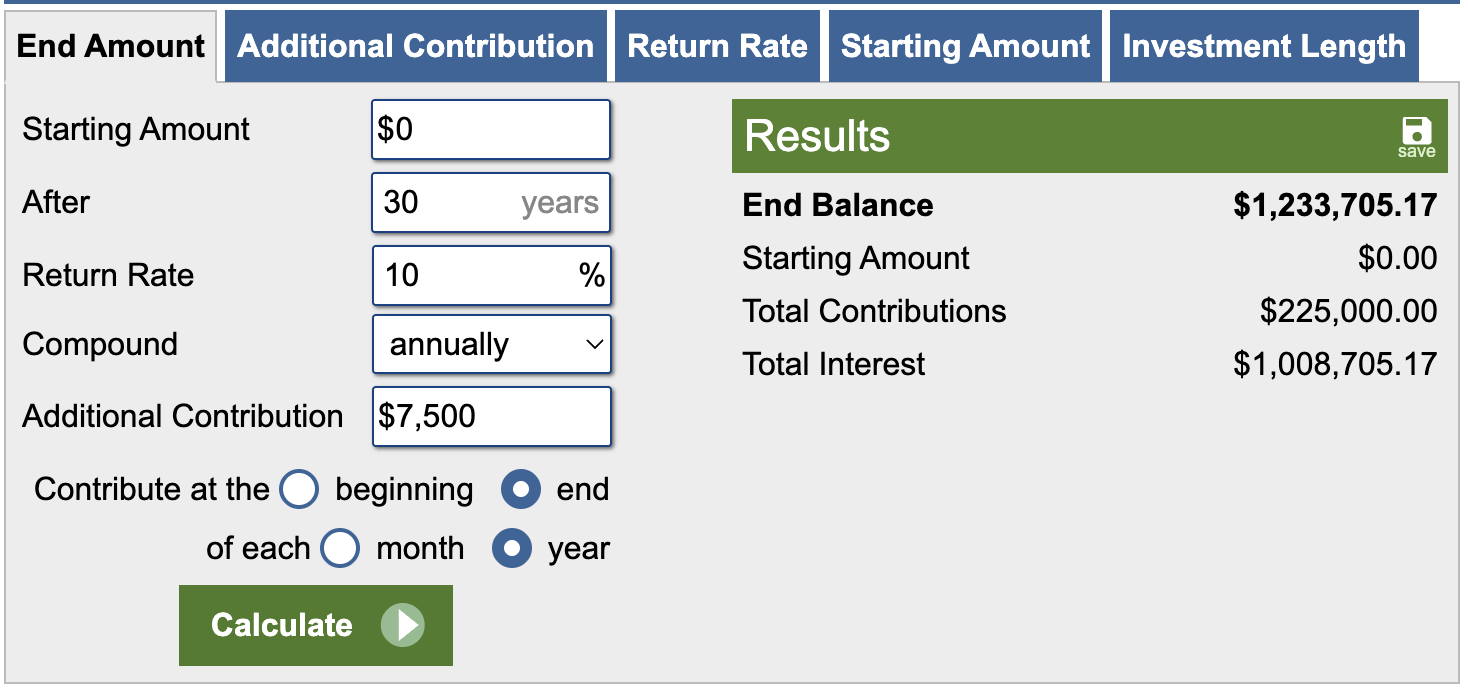

Guess what you would have if you simply put away the maximum IRA contribution into a ROTH IRA every year and invested in a market index fund?

With a $7,500 annual contribution, you would have an over $1.2M account balance, which could generate an annual salary of $100k per year after thirty years. Tax free!

“Compound interest is the eighth wonder of the world. He who understands it, earns it… he who doesn’t… pays it,” – Albert Einstein

If you are at any point in your investing journey and want me to walk you through the best steps for your individual situation, click the button below to set up a free meeting!

Final Thought

It can really be this simple to set yourself up for life. Or you can let other people charge you hefty fees to overcomplicate things.